How Does Profit Sharing Work for Independent Insurance Agents?

Profit-sharing agreements with insurance carriers are a potentially lucrative source of additional revenue for independent insurance agents. These agreements enable agents to earn more on their book of business based on the profitability of their book with the respective carriers.

The details of carriers’ profit-sharing agreements vary, but include performance-based compensation incentives based in part on the yearly loss history of the agency’s clients as well as the agency’s year-over-year growth. Many carriers have minimum premium thresholds for these agreements, making it more difficult for smaller agents to participate in the profit-sharing plans.

Prior to 2020 the performance of carrier profit-sharing plans had been relatively steady, and agents with the scale to meet premium minimums on these plans could count on a meaningful boost in revenue as carriers distributed profit-share payments, usually in the first quarter of each year for prior year performance.

Depending on the financial risk appetite of the agency principal, these funds could represent a meaningful source of working capital for the business – or at a minimum, represent a welcome windfall to kick off the new year.

Why profit sharing has become volatile for independent agents

The years since, however, have been a roller coaster ride for independent insurance agents when it comes to profit-sharing results, particularly in the personal lines space. There has been an unprecedented boom/bust cycle in profit share, primarily driven by policies related to the COVID response.

The years since, however, have been a roller coaster ride for independent insurance agents when it comes to profit-sharing results, particularly in the personal lines space. There has been an unprecedented boom/bust cycle in profit share, primarily driven by policies related to the COVID response.

AM Best reports that private passenger auto liability and physical damage account for about two-thirds of the continually challenged personal lines results experienced among carriers. Combined with losses recorded in homeowners (fueled by above-average cat losses in the last several years), inflationary pressures, and elevated reinsurance costs, personal lines insurers still find themselves in an uphill battle to achieve rate adequacy.

Additionally, social inflation – the amount of costly jury-awarded verdicts against insurers, and the return of those proceedings to courtrooms as the pandemic has eased – continue to adversely affect carriers’ results.

All lines, meanwhile, are subject to the one thing impacting everyone: economic inflation. Price increases have been notably high for goods and services that drive personal insurance claims.

For an independent insurance agent, this volatility is difficult to manage and creates an environment of uncertainty going forward. Is the storm over, or is this the new normal for profit-sharing results?

How agents can improve their profit sharing

Independent agencies truly looking to mitigate the effects of profit-sharing volatility know that performance-based compensation is just one part of the wider solution. There are multiple steps to be taken to establish financial stability independent of the fluctuations of the P&C market, the most important of which are continued revenue growth and disciplined expense management to create a solid foundation that can withstand the impact of profit-share volatility. This is easy to say, but hard to do in practice; joining a member network could be an attractive option.

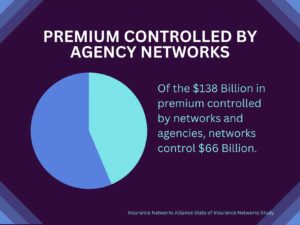

Independent agents have become increasingly aware of the bargaining power represented by networks. Of the 40,000 independent agencies in the U.S. estimated by the Big “I,” 22,000 of them currently are members of agency networks, according to the Insurance Networks Alliance. Of the approximately $138 billion in premium controlled by networks and agencies, networks control $66 billion.

Independent agents have become increasingly aware of the bargaining power represented by networks. Of the 40,000 independent agencies in the U.S. estimated by the Big “I,” 22,000 of them currently are members of agency networks, according to the Insurance Networks Alliance. Of the approximately $138 billion in premium controlled by networks and agencies, networks control $66 billion.

As part of a network, you remove the barriers presented by carrier premium thresholds and expand the number of carriers with which you’re eligible for profit sharing, thus reducing the volatility of payouts while benefiting from the higher compensation levels networks can often negotiate.

However, you need to look beyond carrier contracts. These are table stakes for an agency network. A more impactful network relationship will enable you to grow your business by offering technology solutions, resources, and expertise to take you to the next level of agency management.

This includes assistance with billing and invoicing, to save time and money on administrative tasks; access to a wide range of carriers, which increases your options to serve clients; placement teams that work with you to secure coverage for commercial lines risks; specialists dedicated to growing your agency; vendor discounts on agency management systems; and user-friendly, intuitive technology tools that make your agency money.

Even in a challenging P&C landscape, independent agents have been and will continue to be the most critical members of the insurance value chain. The past three years have tested all business owners, and the typically stable insurance distribution space has not been immune. Although there is no reason to panic, those searching for an edge should look to leverage every possible resource available to help them succeed.